The 50/30/20 Rule: A Budget That Actually Feels Doable

11/8/20252 min read

The 50/30/20 Rule Explained: A Budget That Actually Feels Doable

If budgeting stresses you out or feels too complicated to stick with, you’re not alone. Many people avoid budgeting because they think it means restricting every penny or tracking every small purchase.

But what if budgeting could actually feel simple?

Enter: The 50/30/20 rule.

This popular budgeting method (made famous by Elizabeth Warren) gives your money structure without micromanaging your life.

Let’s break it down.

What Is the 50/30/20 Rule?

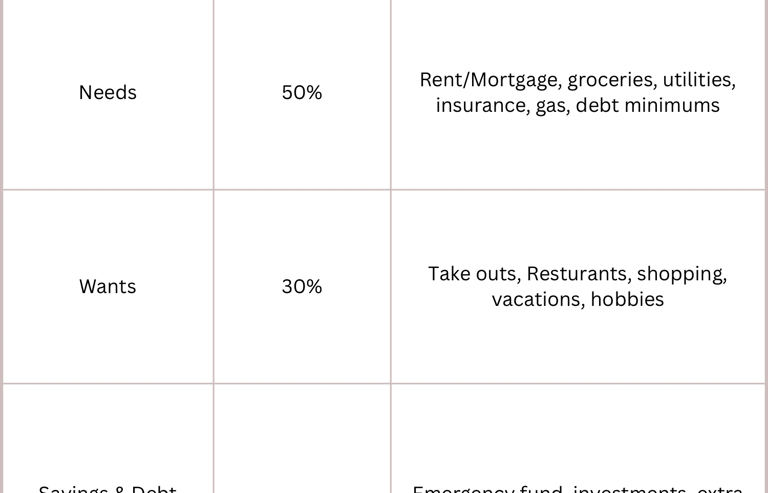

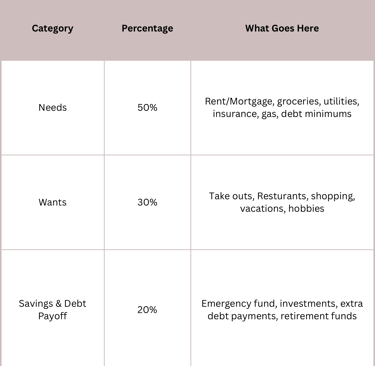

The 50/30/20 rule divides your monthly after-tax income into three categories:

Instead of tracking every purchase, this system gives you spending boundaries.

You don’t panic every time you buy something- you just stay within the category.

Step-by-Step: How to Use the 50/30/20 Rule

Step 1: Calculate Your After-Tax Income

This is your income after taxes, health insurance, and retirement contributions (if they come out automatically).

For example, If you bring home $3,000 a month after taxes:

• $1,500 → Needs (50%)

• $900 → Wants (30%)

• $600 → Savings/Debt (20%)

Step 2: List Your Current Spending

Write down your typical monthly expenses This may include your rent or mortgage, Utilities, transportation, groceries, and or minimum debt payments.

Wants might include: Eating out, coffee, shopping, amazon orders, Netflix, subscriptions, etc.

Savings + Debt payoff might include: Emergency fund, Extra debt payments, and retirement savings (If not deducted from payroll already).

Step 3: Adjust Where Needed. If your needs are higher than 50%, that’s okay! This rule isn’t meant to be rigid, it’s a framework.

If rent is high, reduce “wants”. If you’re trying to reach a big goal, increase savings to 30–40%. If you have debt, put more in the “savings/debt payoff” section. The point is: choose numbers that work for you.

Most budgets fail because they are too detailed. This is why the 50/30/20 rule works especially for beginners.

You don’t have to track every transaction. You just need to make sure you’re within your three category limits. It’s budgeting without the overwhelm.

Budgeting shouldn’t feel like punishment. It should feel like freedom—a plan that helps you confidently say: “I know where my money is going, and I’m in control.” If you’re new to budgeting or overwhelmed by complicated spreadsheets, this method is the perfect way to begin.

BRIGHTER LIFE DESIGN & CO.

Handmade envelopes and budget goods for everyone.

© 2025. All rights reserved.

Privacy Policy

Refund & Return Policy